Guiding economic insights for family businesses in 2026

Posted Feb, 2026

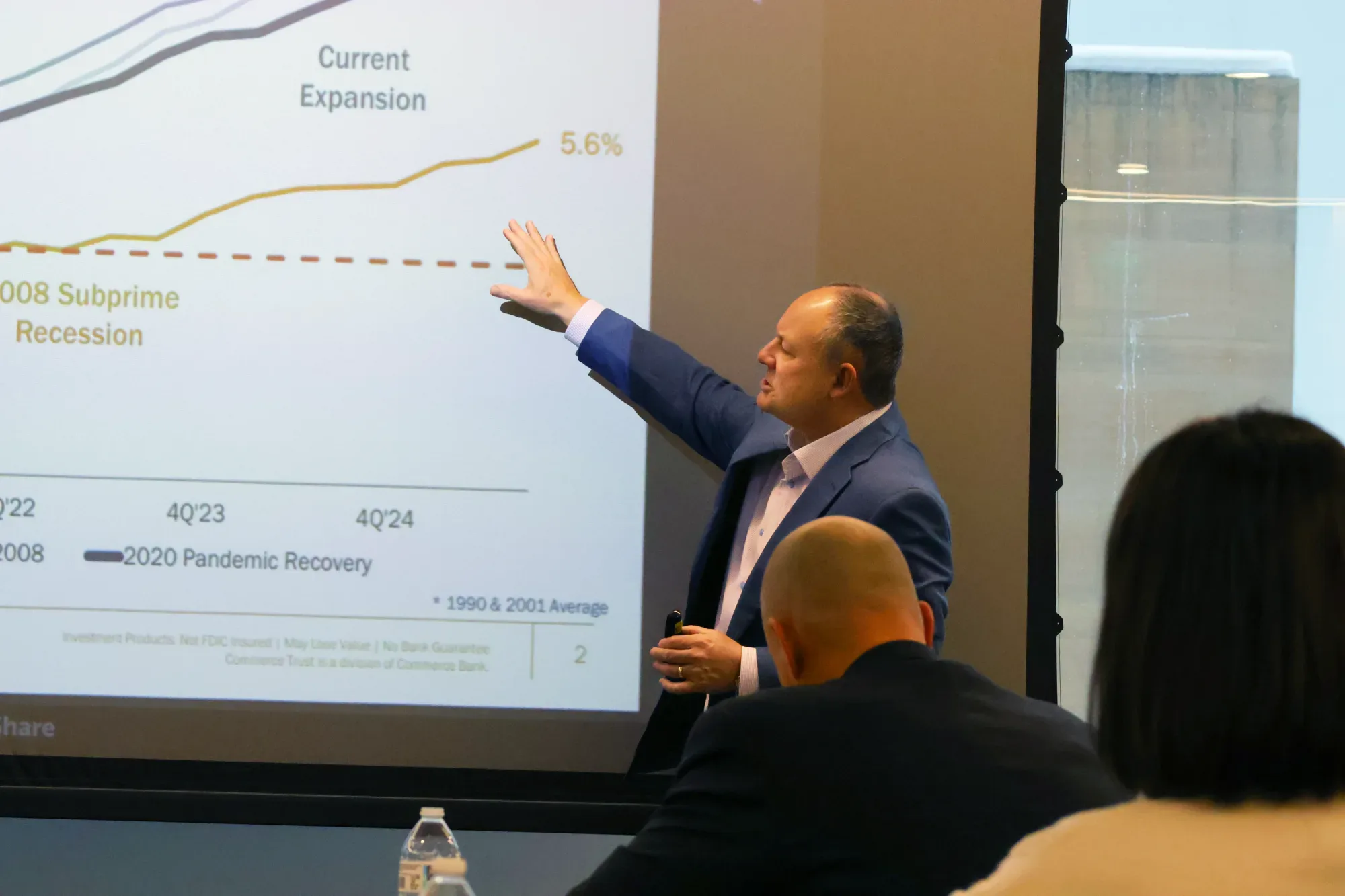

At our recent Economic Update for Family-Owned Businesses workshop provided by Scott Colbert, Executive Vice President of Commerce Bank, one message stood out for family business owners: this is a cooling economy, not a collapsing one; we are currently experiencing a “second wind.”

Below are the five key takeaways and what they mean for family businesses.

This is a cooling economy, not a collapsing one; we are currently experiencing a “second wind.”

1. Jobs Are the Canary in the Coal Mine — and They’re Still Holding

Every U.S. recession has started when net job growth turns negative. While hiring has slowed, layoffs remain lower than hires overall. If people are working, mortgages get paid, customers spend, and businesses can meet obligations.

What family businesses should consider:

- Avoid recession-driven panic decisions

- Focus on retaining core talent rather than aggressive cuts

- Plan for slower growth, not sudden contraction

Bottom line: Labor is cooling, but the economy has not entered recession territory.

2. Banks Care About One Number Most: Unemployment

The strongest prediction of loan charge-offs is rising unemployment. Delinquencies typically increase after job losses occur. Last year, we experienced higher unemployment due to immigration policies and reduction in workforce at the federal level. These two critical factors will most likely not repeat again in 2026, Because employment remains relatively stable, banks are not seeing widespread credit stress.

What family businesses should consider:

- Maintain strong lender relationships and transparency

- Secure or renew credit lines before conditions change

Bottom line: As long as jobs are held, banks stay steady and credit remains accessible.

3. The Economy Is Re-Accelerating — Not Rolling Over

Instead of a traditional slowdown-to-recession path, the economy is showing a modest second wind. This reflects the delayed impact of earlier Federal Reserve rate cuts, continued fiscal stimulus, and increased capital investment driven by accelerated depreciation incentives.

What family businesses should consider:

- Expect uneven demand, not a broad collapse

- Invest selectively in productivity and efficiency

- Use tax incentives thoughtfully—not impulsively

Bottom line: This is a choppy operating environment, but not a downturn-driven freeze.

4. Inflation Explains Most “Growth” — Don’t Be Fooled by Top-Line Numbers

The economy is about 33% larger than it was pre-COVID, but roughly two-thirds of that growth comes from inflation, not real output. Revenue growth alone does not tell the full story.

What family businesses should consider:

- Separate price-driven growth from volume growth

- Monitor margins, unit sales, and cash flow closely

- Re-benchmark performance using real (inflation-adjusted) measures

Bottom line: Revenue growth without margin or volume improvement is not real progress.

5. The Stock Market Is Not the Economy

Markets often perform well when economic growth remains positive, but after multiple strong years, future returns are likely to be more muted. Elevated valuations mean higher volatility and lower forward expectations.

What family businesses should consider:

- Emphasize liquidity, balance-sheet strength, and durability

- Set realistic expectations with family shareholders about returns

Bottom line: Run the business for long-term resilience, not short-term market optimism.

Family Business Alliance strives to help family businesses with the tools, resources, and connections to help businesses succeed. Learn more about our resources including Leading Forward, Succeeding in Succession, and Forging Frameworks of Governance that help to advance family business in our community.

Leave a Reply